The key question here is how much additional value-add does SimplyInsured provide over the online marketplaces being set up under the Affordable Care Act.

A significant part of the broker's value is the high-touch relationship and trust.

The market fit question to me is: if a state marketplace has a decent web portal (like California's http://www.coveredca.com ), what additional value does a private portal offer that NEITHER the official portal NOR an offline broker can offer?

(Don't mean this as polemical by any means; lots of states are not going to have great portals. Just interested in hearing opinions on this.)

I'd argue the ACA will enhance the market for SimplyInsured. Yes, for an individual who wants a basic policy, Covered CA will probably be sufficient and they won't need more help than that. But there are dozens if not hundreds of edge cases.

Some examples off the top of my head:

- A healthy 24 year old software engineer is making $75,000. This means he doesn't qualify for any of the tax subsidies by buying insurance on the exchange. He wants to avoid the $2,500 penalty for being uninsured, but every plan on the Covered CA will cost more than that over 12 months. Perhaps his best option is to buy an individual policy for catastrophic coverage only.

- A small business isn't sure whether it's optimal to insure their employees, or just give them a cash "bonus" and tell them to buy their own policy on Covered CA (similar to what Trader Joe's announced they're going to do with their part-time employees).

- Purchasing insurance on Covered CA is limited only to certain enrollment periods (this is perhaps the biggest misunderstanding, as I've seen various media personalities ask "why wouldn't healthy people just wait until their sick, and then get insurance?" countless times). However, there are exceptions for a life-changing event. Thus, a person who is laid off (thus counting as one of those life-changing events) would like information on whether their best option is to pay for COBRA or buy a policy on Covered CA.

Basically the ACA is complex, but it does turn health insurance into a much more structured and transparent market, which lends itself well to applications like SimplyInsured. Otherwise, what could any sort of system do for my third scenario, for example? All anyone could advise to have them stay on COBRA because they'd probably get screwed by letting it lapse and then trying to get an individual policy.

I agree on the last point: ACA probably actually helps them by making this kind of analysis possible to automate, since it gets the plan data into some kind of commensurable, analyzable form, and simplifies the answers to all kinds of eligibility questions. Once you have a standard format for health-insurance offerings, one analogy could be with air travel, where people build sites like Kayak and Hipmunk on top of ITA's systems. That isn't possible to do adequately if every health plan has its own custom set of terms written in English/legalese.

I'm pretty confident that SimplyInsured's IT would be a huge improvement over the continual problems with the technology of the exchanges. The private sector is far better equipped to actually deliver on the technological promises made by the exchanges. The government is always years behind technologically due to the procurment process. The only reason the NSA has the advantages they do is because much of the technology they use is classified and this not open to potential competition.

There's a role in the government for insurance regulation, however companies like SimplyInsured are needed to actually execute.

I completely agree that the key question for SimplyInsured is how much value they can add once the decent exchanges are up and running. That's why I'm surprised that they've been focusing on California rather than Massachusetts.

Yes, California is a much larger market, but the Massachusetts exchange has been up and running for years. Given that, it seems obvious to me that, for now, Massachusetts is a far better proving ground than any other state for a health insurance business.

I think that there's definitely room for improvement in this space as well as a lot of money to be made because the public exchanges so far are kind of terrible in their usability and access. They will probably improve, but with the lock-in they currently have, there is only incentive to improve enough that the complaints slow down. They get no additional profit for actually making things any better than "possible".

Some previous colleagues of mine just raised 2.6M a couple of weeks ago [1] for a very similar sounding idea [2]. This is a hot space right now with all of the attention on health care because of the ACA and all of the failings of the public exchanges in the press.

They may find themselves with a bigger market than one would think. Correct or not, the general perception of the exchange-based plans is that they are nothing more than extremely limited HMO's (having looked at the plans, this actually seems to be the reality, at least in Nevada). That negative perception, combined with the fines for not having insurance, along with the end of underwriting, will probably lead to a significant spike in people looking to buy private health insurance away from the exchanges. Another large group of people that will refuse to participate in the exchanges will be those that are ideologically opposed to the idea of Obamacare, and those that have grown distrustful of the government's use of data in the wake of the NSA scandal.

It would be nice to know if I should get a Bronze HSA or a Gold PPO based on 1) my medical billing history for the past 1-3 years 2) my past and projected income 3) potentially, my current medical status and good projections about that.

The weird thing about ACA is it essentially turns this into a relatively low range problem; I'm going to be spending $200/mo to $400/mo in premiums, and I'm never going to be out of pocket more than $6350 on top of that. So even if I do exceptionally well, it's maybe a $200x12 - $3300x0.35 (tax savings on HSA) cost vs. a $400x12 plus epsilon cost vs. ($200x12 + $6350). Which isn't enough to really care that much, since most likely it's within $1-2k/yr regardless of which plan I pick. And I doubt your picking would be that much more accurate than a general WAG based on "do I often go to the doctor?"

Given the glacial speed of reform in the U.S. (something like these new exchanges have been in the works since Nixon proposed a similar system), I would put that fairly far down the list of risks a small startup should worry about. A much bigger risk imo is just whether the value-add of their tools over the official state websites will be enough to gain traction.

Hard to imagine a motivated startup NOT being able to offer more value. State-run websites almost uniformly have abysmal usability, are slow, and are ugly. Sure there are exceptions but I think there will always be a lot of niches, or even bigger openings, to fill. And when you're talking about a market that is going to be compulsory for every adult, even a niche can be quite rewarding.

I have to be honest: as an IT professional, I'm extremely impressed with how well designed https://www.healthcare.gov/ is. I understand its having some problems under load, but I think we're all a bit forgiving here about traffic problems when you're receiving 5 million visitors/day in traffic.

....which would explain why every first world country uses it except the US?

I'd much prefer we don't devolve into a political argument. My question, I thought, was relevant due to ACA kicking in, which is the first step towards universal healthcare/single payer in the US (which would eliminate the business model in question).

The US is 5-10x larger in population than the other single-payer-ish systems usually cited. (And, more culturally/politically/geographically varied.)

Also, we in the US tend to have bigger problems running giant federal bureaucracies, compared to these other smaller, more-unified nations. (How many government shutdowns have they had in the past 40 years?) Our existing single-payer-ish health bureacracies, like Medicare, suffer more fraud and cost-problems, and have a harder time enforcing steely-eyed rationing (aka "death panels") than elsewhere.

These smaller systems also benefit as free-riders from positive externalities thrown off by the United States' eccentric overexpenditures - like drug and new-treatment beta-testing. (If we become more like them, their own medical indicators could get worse.)

So the argument can't just be, "make it work like over there", when nothing here works quite like there, and our challenges of scale, culture, and politics are larger.

> The US is 5-10x larger in population than the other single-payer-ish systems usually cited.

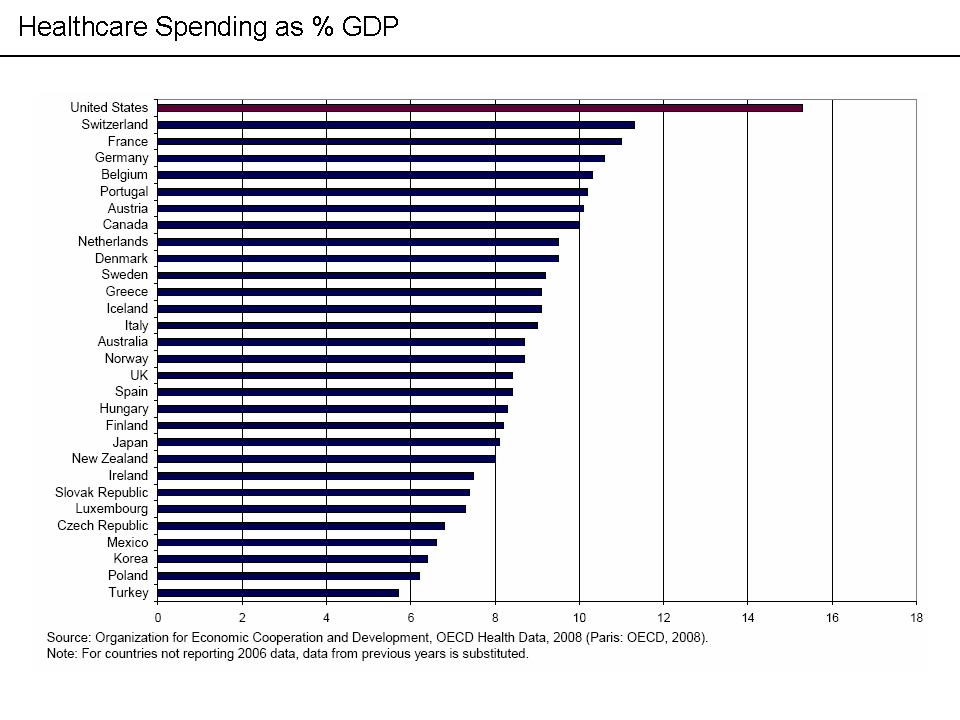

Which doesn't explain the vastly higher per capita (and even per GDP) costs.

> Also, we in the US tend to have bigger problems running giant federal bureaucracies

That doesn't explain why the US costs (again, per capita or per GDP) are still higher than the total costs in many countries providing universal coverage even if you exclude the slightly-less-than-half of US spending that is public spending.

> Our existing single-payer-ish health bureacracies, like Medicare

Medicare isn't single-payer-ish, as for decades there has been policy to move from traditional single-payer-ish "Original Medicare" to (usually partially, with a personal premium as well) publicly subsidized private insurance "Medicare Advantage" plans.

> These smaller systems also benefit as free-riders from positive externalities thrown off by the United States' eccentric overexpenditures - like drug and new-treatment beta-testing.

Er, a lot of drugs and new treatments are tested and accepted overseas before they are in the US.

You're right: our costs are off-the-charts. There's something about our culture and politics that's making that happen, even in a system with centralized price-setting like Medicare.

If you can't answer why Medicare seems to do worse than your favorite "single-payer-ish" models, you haven't explained how making the entire system into a single-payer system, a bureaucracy of unprecedented size, will improve things over a smaller bureaucracy that's failing at controlling costs.

Some drugs and new treatments start elsewhere. A disproportionate number start in the US. Fancy new (and often unnecessary) treatments are one of the things driving our costs up.

"There's something about our culture and politics that's making that happen, even in a system with centralized price-setting like Medicare"

It's not a difficult puzzle: nobody in our system is incentivized to care about costs. The insured consumer never sees the cost, the physician is incentivized to be cost-blind when choosing treatment options, and the insurance companies pass the costs back to employers, who don't get any say in treatment. The only other people who know what health care costs are unemployed and/or poor, and well...screw them, right?

You couldn't possibly choose a worse economic model for allocating health care. Medicare is much cheaper and more efficient than employer-based healthcare, but it can't overcome the structural expenses created by a system dominated by people who are almost totally cost-insensitive when it comes to their health.

And yet they don't. Do you know that the cost of prescriptions can vary greatly between pharmacies? Of course, you only pay your co-pay, but your insurance company pays the difference.

When's the last time you comparison-shopped your prescriptions or other medical services?

Drugs aren't the best example since they are inexpensive (at least the ones I've purchased). But if I had a more expensive surgery where I was on the hook for 20-40%, I might be incented to negotiate or shop around. And you'd certainly think the insurance company would be highly incented to negotiate.

"Drugs aren't the best example since they are inexpensive (at least the ones I've purchased)."

There are some very expensive drugs, and they're not uncommon. For example, valcyclovir is a very common anti-viral drug, and costs something like $300-400 per course. The similar drug acyclovir is $20 as a generic, but is more annoying to dose. As a result, doctors will nearly always prescribe valcyclovir over acyclovir. For patients with a chronic infection, that's a mundane decision with an impact of tens of thousands of dollars per year. But unless you're a doctor or a pharmacist, you'd probably never know about the choice.

Insurance companies pass these costs on to the risk pool first, then onto employers. By the time the cost increases hit you (through employers cutting or reducing your health benefits), the implications are so far removed from the initial expenses that there's no way to close the cycle.

But better at cost control than private insurance in America, with much better cohorts. They're in America, medicare can't get you british-cost healthcare.

> The US is 5-10x larger in population than the other single-payer-ish systems usually cited. (And, more culturally/politically/geographically varied.)

I see this argument all the time, and never an elaboration.

I understand going from 1,000 to 1,000,000 people incurring growing pains, but I have a hard time understanding why people seem to think a system that works for 80,000,000 people in Germany wouldn't be scalable to 300,000,000.

…isn't quite single-payer, more like a "public option".

…has far more labor-business-government cooperation than the US.

…has the oldest tradition of social insurance, but still their current system was the result of gradual expansions over many years.

…runs lots of government services better than the US.

…is only half the area of Texas, but that area is as population-dense as Maryland (our 5th densest state).

Why can't any 300 million people in Africa just adopt US-levels of public services by willpower and legal fiat? Why can't the US make our 50-million-member Medicare as efficient as the German system? These structural, historical, cultural, and political path-dependencies matter.

"Make it work because I don't understand how it couldn't" isn't a good basis for the largest nationalization experiment ever.

> ....which would explain why every first world country uses it except the US?

Every first world country except the US has something approximating universal coverage, but not all of them use single-payer (or even a single basic coverage insurer with supplemental coverage from other payers.) Compulsory-purchase insurance models similar to those in the ACA (but, you know, actually universal) with private insurers are not unheard of (e.g., Switzerland uses that model)

Switzerland's is interesting in that it goes a step further than Obamacare and really makes it compulsory, rather than simply fining you for not having insurance. A colleague was a postdoc there for a while and didn't understand the system, and after ignoring a few letters telling him he needed to buy insurance, he got a follow-up letter telling him that, as he had not yet enrolled in a plan, a default one had been chosen and he was now enrolled in it.

I would like to point out we're also significantly more overweight, have higher rates of heart disease, have a quickly aging population of baby boomers etc.. Your argument is not logical as there are plenty of other reasons we have higher healthcare costs other then that we're not single payer.

> I would like to point out we're also significantly more overweight, have higher rates of heart disease, have a quickly aging population of baby boomers etc..

Those are all, arguably, consequences of the poor access to health care in this country and the short-term incentives in this country to delay care. IOW, they are products of the system that we pay more for (per capita or even per GDP -- or even either way only considering public expenditures and excluding the private costs) than first world countries that provide universal coverage through government single-payer systems.

I see this argument a lot: people go without care, or delay early treatments that would be cheaper, because they can't afford to go to the doctor. I'm sure this is true to a degree, but making terrible diet choices, being sedentary, and being 100 lbs overweight is not a consequence of not having health insurance.

And I really don't see the avoidance of primary care being primarily financial either. A yearly routine physical is not very expensive, and is often free at many public health clinics. Likewise common preventive care like flu shots, pap smears, and prostate exams.

A big reason a lot of people don't go to the doctor is that they don't like going to the doctor. I'm in that group. Having insurance doesn't change that.

There is a huge cultural difference between almost every single payer nation and the US. For example, I haven't seen a regular doctor in 3 years for any kind of check up, because I'm uninsured. Meanwhile, I have friends in Canada that get quarterly or even monthly checkups. It isn't even a cost thing, they say it is cultural - their parents and peers expect them to regularly see a doctor to make sure nothing is wrong with them, and if they sneeze wrong they see the doctor.

I dislocated my knee this spring and reset it and just stayed in bed for 2 weeks. Never saw a medical professional, because they would want to x-ray (it might have broke, it was much more painful than a normal dislocation to me, and swelled huge for a while) and I'd be stuck with a $3 - 5k bill minimum just for that, combined with any treatment, and I'd laugh if they'd want me in physical therapy for it.

So it isn't just about not haivng a doctor to say 3 bic macs a day is bad for you, it is that in most other places people do see their doctors, regularly, and for most issues, beucase it doesn't bankrupt them. That adds up over a lifetime.

"But I think the biggest single driver is our fee-for-service system that rewards volume instead of value and quantity of medical services instead of quality. And as a result, we end up doing a lot of things that cause more harm than benefit for patients."

Also:

"What that dramatic variation tells us is that there's a lot unnecessary medical care that's being delivered and a lot of room to eliminate some of that wasteful spending."

> ....which would explain why every first world country uses it except the US?

Which is why almost every country outside of the US has a lower standard of care than we do. I'd be fine if we had a "minimum safety net" which covered catastrophic care, but thats not what was put into law. I also think a government mandated requirement to purchase a commercial product is probably not a good thing.

> Which is why almost every country outside of the US has a lower standard of care than we do.

You just like to make up shit I see. Every country that provides public healthcare has a higher standard of care than we do because for 10's of millions of American's there is no care at all beyond emergency care. People die daily for lack of health care in this country, to call that a higher standard than countries with public healthcare is beyond absurd. Our system has a fantastic standard of care for those with money, it has shit for care for the rest.

> Which is why almost every country outside of the US has a lower standard of care than we do.

Uh, where do you get that from? The JAMA study, one of the most comprehensive such studies done, concluded that the US health care outcomes are far worse than comparable nations, yet we pay significantly more for it.

The biggest reason we pay more is that provider costs are much higher than the GDP-adjusted average. $500,000,000,000 more. (And before you say it, that's factoring out defensive medicine and the results of tort reform.) A lot of that has to do with insurance companies inability to negotiate reasonable rates with the providers. And of all the insurers in the US, which is the only one that can and does negotiate reasonable rates? Medicare.

I think many/most would disagree with your contention that other countries have a lower standard of care. It's particularly annoying that your so matter of fact about it.

{kind=link}

A significant part of the broker's value is the high-touch relationship and trust.

The market fit question to me is: if a state marketplace has a decent web portal (like California's http://www.coveredca.com ), what additional value does a private portal offer that NEITHER the official portal NOR an offline broker can offer?

(Don't mean this as polemical by any means; lots of states are not going to have great portals. Just interested in hearing opinions on this.)

[Edit: making CA link a real URL]